How to Pay Off Credit Card Debt

If you feel overwhelmed by credit card debt, you’re not alone. According to a TransUnion report, the average cardholder debt is over $6,000. Yikes!

However, it’s never too late to end the cycle of minimum payments, high interest rates, and fees. Once you do, you can focus on bulking up your retirement or emergency fund savings, and investing for the long term.

To bring your debt under control, we created a step-by-step worksheet to help you get organized and ready to commit to a payoff plan. We also spoke to financial experts who shared their best advice for tackling debt.

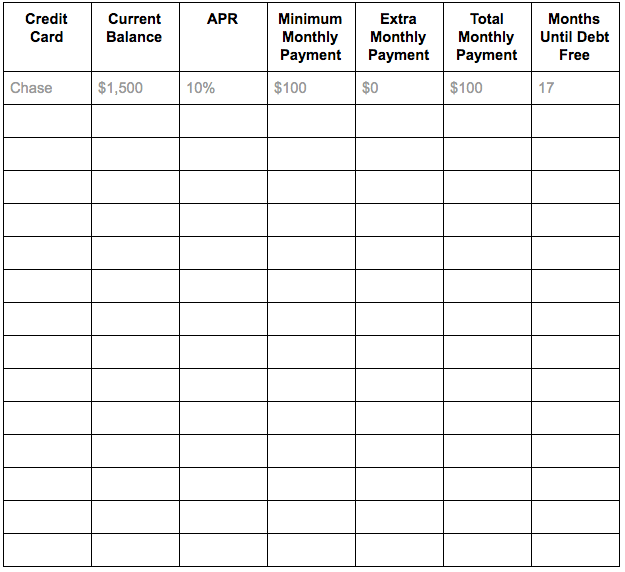

Credit card payoff worksheet

When you’re deep in debt, it's hard to see the light at the end of the tunnel. That’s why choosing and working toward a payoff date can be so effective, and that's exactly what our worksheet can help you with. Your payoff date is the precise day that you will pay off all your cards. You can calculate the date by determining when your monthly payments will bring your balances to $0. This gives you a concrete goal to work towards and allows you to imagine your life without debt.

To determine your payoff date, use the worksheet below to calculate the number of months it will take to pay off your debt.

- Make a list of every credit card account you have open.

- Write down the most recent balance on each of those credit cards.

- Find the APR for each account; it will be on your account statements or listed with your other account information online.

- Finally, list your required minimum monthly payment.

Now it’s time to see how long it will take to become debt free. Plug the numbers into a payoff calculator and write down how long it will take to pay off the cards. Is it eye opening? Making only the minimum payment means your payoff timeline will be stretched long into the future. Use that realization as motivation. Consider making an extra contribution above the minimum payment each month. The more you pay, the sooner you’ll be debt-free. Recalculate your payoff timeline based on the total monthly payment. Notice how the timeline decreases as your extra payment amount increases.

Steps to pay off credit card debt

For many people, paying off debt is easier said than done. It’s hard to know where to start, and it can be even harder to stick to a plan once you do.

Here are six steps you need to tackle your debt, as well as expert advice to guide you along the way.

1. Take stock

Start by taking an overview of your debt. List your credit cards and their balances—this makes you take accountability for every credit card you own.

Next, follow the worksheet steps to calculate how long it will take to pay off each credit card. Keep in mind that the longer you take to pay off your balances, the more you’ll pay in interest. To drive home the point, calculate exactly how much interest you will pay. Ask yourself if the purchases you’re making are worth it.

Tips from the pros

Todd Christensen, education manager at Money Fit by DRS

Todd Christensen stressed that to reduce debt, the first thing to do is stop adding to it.

“You can't get out of a hole unless you stop digging it deeper,” Christensen says. He explained a clever idea for minimizing the chances of overspending with a credit card. “While cutting up the card is probably more effective, you can put it on ice, literally,” he said. “Place it in a cup of water and then freeze it. Even with a blow dryer, the extra work and the ten minutes or so necessary to melt the ice might be enough to get you through the impulse to make an unplanned purchase.”

Lisa Hebert, founder of MoneyMindedMom.com

Lisa Hebert, the founder of a personal finance blog, suggested that the best piece of advice when trying to pay off debt is to mentally prepare for the long journey. “You need to change the way you think about money and reprogram your thoughts and habits,” she said. “You need to start valuing money for what it’s worth. Not that it’ll buy you happiness, rather that it’s holding you back from achieving it.” She added that once you achieve this, “you’ll realize that sticking to a budget or giving up certain things to get out of debt is not as difficult as they seemed to be.”

Justin Ehrhardt, “The Bearded Financial Pro”

Ehrhardt, an entrepreneur in the financial services industry, emphasized the importance of creating a strict budget to learn how to create a mindset and habit of not using credit cards. By creating a budget you’re more likely to rely on this tool to get out of debt and less likely to fall back on old habits.

Ehrhardt recommended Google Sheets. He uses the application to keep a budget on his phone and track what he’s spending and where.

“People will typically use credit cards as an income buffer because they overspend,” he said. “A great way to not even have spending on a credit card is to eliminate it from all saved transactions online where your card can be auto filled and also stop carrying your credit card around with you.”

2. Consider consolidating or a balance transfer

Consolidating debt and transferring it to a new card with a low interest rate is one tactic for tackling debt. It can work like a charm, but only if done responsibly, financial experts warn.

Tips from the pros

Riley Adams, CPA

Adams, a certified public accountant and financial analyst, understands that it’s not an easy process to get out of credit card debt. Between the high interest rates and late fees, it hurts even worse to know that your balance will only continue to grow without a sound debt management plan.

Luckily, there’s a legitimate hack of either consolidating your multiple credit card debts into a single loan or to balance transfer your debt to a new credit card with a low introductory APR and no annual fee.

“If paying off debt will span multiple months or even years, it might be worth considering a personal loan for a lower interest rate,” Adams said. “If you can find a low-cost (0% interest with nominal balance transfer fee less than 3%) balance transfer on a credit card offer, it may make sense to apply for that to transfer the balance and make as many payments as possible before that balance transfer starts costing you more money.”

What this means is that you transfer your debts to a card without interest for an introductory period, typically six months to a year. This allows you to put more money toward the principal amount instead of merely paying interest each month.

Uri Abramson, co-founder of OverdraftApps.com

Abramson, a cofounder of the personal finance blog OverdraftApps.com, agrees with the balance transfer method. However, the solution isn’t the right choice for everyone. Here’s why, he writes:

- You must have access to new credit.

- You must stop making new debt.

- You must be able to schedule and execute your monthly payments––religiously! Even with 0 percent interest, it might not be easy. Say, you have a $12,000 debt and a 12-month 0%intro period. You would have to pay roughly $1,000 a month without borrowing more money from a credit card––any credit card you hold!

- You must pay off your balance completely by the time the regular APR hits OR…

- If you can't pay it off completely, make sure to find a new intro 0%balance transfer credit card to transfer the remainder of your debt.

The underlying problem with credit card debt is continuing to spend and rack up debt. “If that doesn't change, the vicious circle will return,” he said, adding that “after you clean up, there are no carrying balances anymore.”

Reminder: don’t abuse your new 0% APR cards either, because at some point the interest will begin to accrue.

3. Choose a repayment method

Two of the most popular methods of paying off debt are the "snowball" and "avalanche" methods.

The snowball method is a debt reduction strategy where you pay off the debt from the smallest to the largest, gaining momentum as you knock out each balance. When the smallest debt is paid in full, you roll the money you were paying on that debt into the next smallest balance.

The debt avalanche is a popular repayment strategy in which a borrower works toward paying off high-interest debt first while making minimum payments on other loans. The idea is to target high-interest debt that is likely to cost you the most money in interest payments.

Growing interest can make it tough to climb out of debt, so zeroing in on this debt can help tackle this issue and make real progress.

Tips from the pros

Todd Christensen, education manager at Money Fit by DRS

While the snowball and avalanche methods tend to be the most talked about, Christensen suggested a little-known third method: the credit card level pay method.

“If you absolutely cannot come up with any additional payment above the current minimum payment due, make this month's minimum payment the amount you send for all future bills, even as the credit card company begins asking you for less and less,” he explained. “Whereas minimum payments will take you 15 to 25 years to pay off your debt, the level pay method will have you out of debt in six or seven years.”

4. Free up money for repayment

How can you find additional money to put toward debt? Paying off a credit card quickly means being creative. Our best suggestion: cut costs.

If you are overspending on food a good way is to avoid eating out. Cooking at home and using coupons can help you reduce your grocery bill. Even if it’s hard, it’s worth it. Target your money weakness, whatever it is, and put a hold on spending. The extra money saved can be used to make additional credit card payments.

Another option is to consider an additional source of income. Whether you decide to pick up an extra shift, work freelance on the side, sell your belongings, or monetize a hobby, adding another source of income can help, no matter the amount. An extra $20 each week can go directly toward a credit card payment. That’s about $80 a month, or $1,042 a year!

Tips from the pros

Justin Ehrhardt, “The Bearded Financial Pro”

The most important reason why you should allocate more of your income to the repayment of credit card debt beyond minimum monthly payments is simple: interest.

“When it comes to your credit card bill, paying the minimum on your bill will predominantly pay for the interest accumulated for that month,” Ehrhardt explained. “For example, a person may have a $500 credit card bill and their interest for that month could have accumulated up to $20. If your minimum payment is $25, you're mainly paying $20 straight for interest and only $5 to go to the principal. Credit card companies want you to make minimum payments because it will allow them to keep the debt on longer, which in turn makes higher interest and makes your payment longer over a given time.”

While freeing up money for debt repayment is hard, Ehrhardt stresses that every little bit makes a difference.

“Some families may have tight monthly budgets and feel like they cannot contribute more to their debt,” he said. “Even simply adding $5 to their monthly amount above the minimum can drastically change the length of time for their card,” he urged.

Todd Christensen, education manager at Money Fit by DRS

Christensen agrees. “Take 10 percent of your grocery spending, dining out expenses, coffee shop purchases, and entertainment for the month, and set up an automatic payment from your checking account in that amount,” he suggested. "We call this your PowerCash, and most households can come up with $50 to $200 a month extra to accelerate credit card repayment.”

5. Choose a monthly repayment amount

The best way to decide on a monthly repayment amount is to choose a date in the future as your credit card payoff goal. Use the worksheet to calculate different repayment timelines based on the amount you’re willing to pay. Make sure that you can meet the minimum each month, but plan for extra payments if you can.

Tips from the pros

Deborah Sweeney, CEO of MyCorporation.com

Prevention is the best method, according to Deborah Sweeney. She said that when paying off credit card debt, she advises to only put on the card what you know you can pay off in full. She stressed spending responsibly and said, “do not look at your credit card as a way to buy more than you should or can.” Further, she said to “pay off your balance in full as quickly as you can to avoid paying more in high interest rates.”

Karen Ford, master financial coach

Karen Ford suggested contacting your creditor and discussing the terms of your credit line. “Ask if they will give you a discount for paying it off early,” she said. “Many times, card companies will give a 10-20% discount for early pay off.” If not, at least “pay an extra $5 - $20 or whatever you can each month. This will allow you to pay down that debt even more quickly.”

6. Stick to it

Let’s face it: paying off credit card debt is daunting. It’s a long process with several hurdles and no end in sight. Sometimes you need a little help, and there are many support organizations out there that can provide knowledge, resources, and encouragement to help you meet your goals.

Tips from the pros

Linda Ruescher, author, and speaker on chronic illness

Linda Ruescher discussed options available to those suffering from credit card debt. While she isn’t a credit expert, she emerged from serious medical credit card debt with the aid of a counseling service.

“When one is overwhelmed with credit card debt, simple fixes like hiding credit cards, creating a strict budget, or doing balance transfers are merely band aids on a hemorrhage,” she said.

The first solution is self-examination. It’s crucial to address how one got into an unmanageable amount of debt to begin with. “Some folks get overwhelmed by medical expenses,” she said. “For medical expenses, one might be able to negotiate with the provider,” she explained.

The second part of the solution is to find a free service that will assess any financial situation, create a budget and debt management plan, and negotiate with creditors on the client’s behalf. Ruescher explained her experience with a counseling service. “Clients make one payment to Consumer Credit Counseling and the agency distributes the payments to creditors.” She added that “a nice benefit is that clients no longer receive dunning calls.”

Bottom line

If you find yourself in a never-ending cycle of credit card debt, don’t get overwhelmed. Fill out our worksheet to take stock of the situation and know your current balances. Consider consolidating or transferring the balance of your credit cards to get the best interest rate possible. Choose a repayment method and free up extra money to put towards a repayment plan. Start repaying your credit card debt on a monthly basis while making sure to not rack up more debt. Tap into free counseling resources to stay on track.

Uri Abramson is a co-founder of the personal finance blog OverdraftApps.com, with a long history of working in the banking and fintech industry. He also held key technical and management roles in international fintech startup companies. As one of the first software engineers of Payoneer, he was lucky enough to learn the ins and outs of the payments industry, from the inner workings of payment processors and gateways to the consumer level of financial services (banking, credit cards, etc.).

Riley Adams is a licensed CPA in the state of Louisiana working as a senior financial analyst for a Fortune 500 company in New Orleans. He has a personal finance blog dedicated to helping young professionals find financial independence at WealthUp.com.

Todd Christensen, MIM, MA, author, and accredited financial counselor, is education manager at Money Fit by DRS, Inc., a nationwide nonprofit financial wellness and credit counseling agency. Todd develops educational programs and produces materials that teach personal financial skills and responsibilities to all ages. Having facilitated nearly two thousand workshops since 2004 on the fundamentals of effective money management, he based his first book, “Everyday Money for Everyday People” (2014), on the discussions, tips, stories, and ideas shared by tens of thousands of individuals and couples in attendance.

Justin Ehrhardt, aka The Bearded Financial ProTM, has been an entrepreneur in the financial services industry as well as an Air Force Veteran and previous firefighter. He was originally recruited into the financial industry by an expansion director in the state of Georgia. Ehrhardt started his financial practice in Duluth, Georgia after becoming inspired by his personal experience as a client. His passion for education and empowerment of families who had been neglected, overlooked, or misrepresented by the financial industry fueled his passion. Ehrhardt’s strength is to teach families and business owners how money works and how to better manage their money in simple, common terms.

Karen Ford is a master financial coach, public speaker, entrepreneur, and author at KarenFord.org who has coached people with a variety of money issues; from just $500 in debt to $800,000 in debt. She has coached folks with up to 86 credit cards and taught them how to pay down and pay off those credit cards in record time.

Lisa Hebert founded MoneyMindedMom.com, a personal finance blog where she shares tips on getting out of debt, saving and budgeting money. Her mission is to help others manage their finances better so they can pursue a better life without financial stress.

Linda Ruescher is an author and speaker whose work focuses on helping people live successfully with chronic illnesses at CopingWithChronicIllness.com.

Deborah Sweeney is the CEO of MyCorporation.com which provides online legal filing services for entrepreneurs and businesses, startup bundles that include corporation and LLC formation, registered agent services, DBAs, and trademark and copyright filing services.

Please note the below article contains links to external sites outside of OppU and Opportunity Financial, LLC. These sources, while vetted, are not affiliated with OppU. If you click on any of the links you will be sent to an external site with different terms and conditions that may differ from OppU’s policies. We recommend you do your own research before engaging in any products or services listed below. OppU is not a subject matter expert, nor does it assume responsibility if you decide to engage with any of these products or services.