Compound Interest: BFF or Worst Enemy?

It’s been said that mathematical genius Albert Einstein once described compound interest as, “the eighth wonder of the world.” Einstein further stated, “He who understands it, earns it… he who doesn't… pays it.”

What is compound interest?

Let’s start with a definition of interest.

Defining interest

Interest is money paid by, or charged to, people in exchange for borrowing money. A lender will earn interest on the money they loan, and a borrower will pay interest on the money they borrow, such as from a loan or credit cards.

Conversely, a person who saves or invests their money with a financial institution can also earn interest on the funds they deposit with that bank.

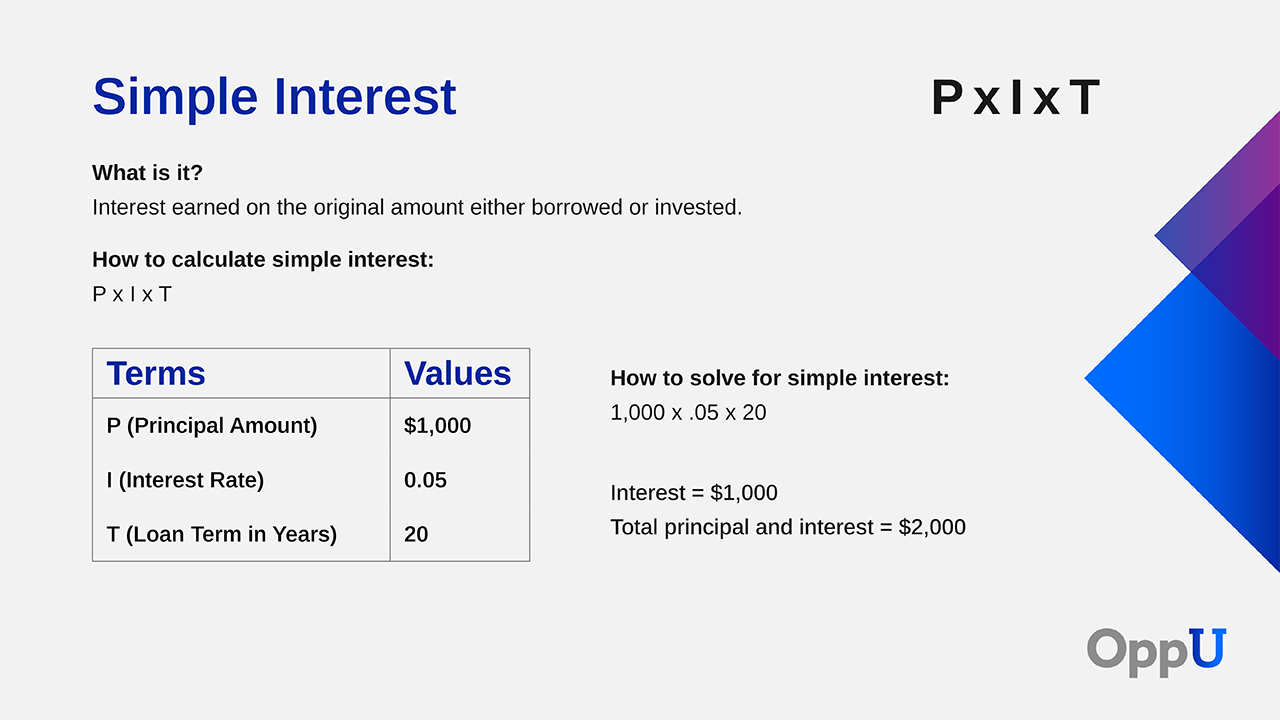

How does simple interest work?

To calculate simple interest, take the principal amount and multiply it by the annual interest rate and the loan term. For example, if you took out a $2,000 loan with a loan term of two years and a 5% interest rate, you’d pay $200 in interest. See below:

$2,000 (principal amount) x 0.05 (interest rate) x 2 (loan term in number of years) = $200

The total amount you’d pay on the loan would be $2,200.

$2,000 (principal amount) + $200 (total interest) = $2,200

Defining compound interest

Compound interest is interest earned on interest. Depending on the type of account, interest can accrue daily, monthly, quarterly, semi-annually, or annually on the original investment (called the principal) and on previously credited interest.

“People should know that compound interest makes money grow faster. It allows you to build interest on your interest, whereas simple interest is just based on the principal,” says Micah Bender, a School Business Administrator.

The magic of compound interest

Most people don’t become wealthy from their paychecks alone. They do so with a combination of earnings, regular savings, and compounding interest over time. Stated another way: Their money makes money. Compound interest packs a saver’s principal with power.

“Over time, as more interest adds to the original investment, earnings may seem to magically increase,” says Laura Hendrix, Ph.D., an associate professor for personal finance and consumer economics with the University of Arkansas Cooperative Extension Service. “That’s why you may sometimes hear it referred to [as] the ‘magic of compounding.’”

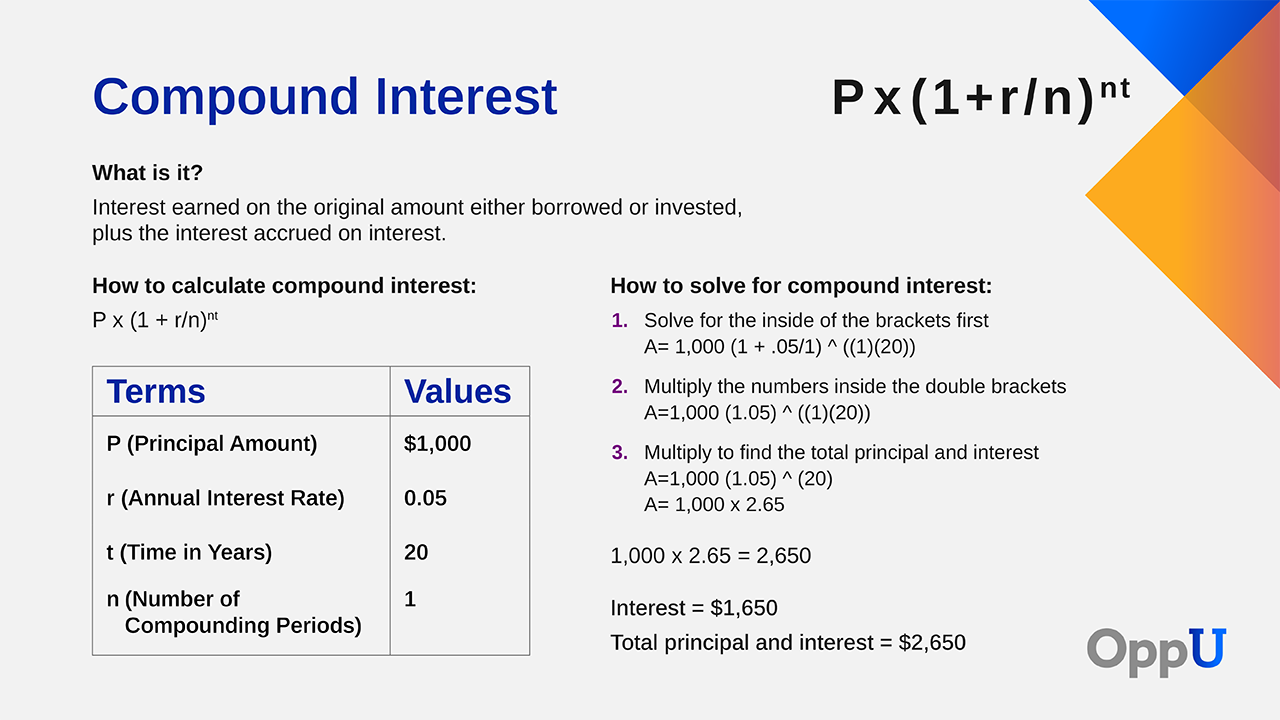

Compound interest formula

With simple interest, if you had an initial amount of $1,000 in a high-yield savings account, and it earned 2% interest annually, at the end of the first year you would have $1,020. What would happen if that same initial investment earned compound interest over five years?

To calculate compound interest, use the following formula:

A = P x (1+ r/n)nt

- A = Principal amount plus interest

- P = Principal amount

- r = Annual interest rate

- t = Time in decimal years

- n = Number of compounding periods per unit of time

With compound interest, you earn interest on your interest. At the end of the fifth year, you would have $1,104.08.

A= 1,000 x (1 + .02/1)(1)(5)

- P= $1,000

- r = 2% ( .02 as a decimal)

- n = 1 year

- t = 5 years

To break it down a bit more simply, follow the steps in the images below to calculate simple and compound interest:

Small, regular savings deposits over a long enough period of time can grow to five-, six-, and even seven-figure sums. The amount of money you save is less important than having a regular saving habit. As your bank account balance grows, you earn interest on increasingly larger sums.

Some compound interest math

“Compound interest is the foundation for building savings over the long term,” says Jesse Ketterman, Ph.D., an extension educator and accredited financial counselor with the University of Maryland. “It can help you by reinvesting the interest you earned on your savings.”

The good news about compound interest is that it works for everyone regardless of income, occupation, and education. If you set aside any amount of money into a savings or investment account, compound interest can be extremely beneficial.

To prove this point, below are actual numbers that assume a 6% average annual rate of return with 6 different amounts of weekly savings ranging from $5 to $100. The table shows the savings you could achieve by age 65 with compound interest on your side.

| Age | $5/Week | $10/Week | $25/Week | $50/Week | $75/Week | $100/Week |

| 25 | $ 43,149 | $ 86,298 | $ 215,745 | $ 431,490 | $ 647,234 | $ 862,979 |

| 30 | $ 30,869 | $ 61,737 | $ 154,344 | $ 308,687 | $ 463,031 | $ 617,374 |

| 35 | $ 21,764 | $ 43,529 | $ 108,822 | $ 217,645 | $ 326,467 | $ 435,290 |

| 40 | $ 15,015 | $ 30,030 | $ 75,074 | $ 150,149 | $ 225,223 | $ 300,297 |

| 45 | $ 10,011 | $ 20,022 | $ 50,054 | $ 100,109 | $ 150,163 | $ 200,218 |

| 50 | $ 6,301 | $ 12,602 | $ 31,505 | $ 63,011 | $ 94,516 | $ 126,021 |

| 55 | $ 3,551 | $ 7,101 | $ 17,754 | $ 35,507 | $ 53,261 | $ 71,014 |

Several noteworthy patterns are evident:

Time is money

The more someone saves each week ($100 vs. $5) and the longer they save (40 years vs. 10 years until age 65), the more money they will accumulate.

Age matters

Note the widening gap between account balances at different ages and dollar amounts.

Baby steps work

Any amount of savings is better than no savings at all and can snowball into a large lump sum. Even saving $5 a week will result in a five-figure sum if you start at or before age 45.

The flip side of compound interest

Just like compound interest can grow your savings, it can also grow your debt and work against you; this is when compound interest can be your worst enemy.

Over time, the cost of interest can be significant. This is especially true for debts that have a long pay-off period (e.g., home mortgages, student loans) or in circumstances where you are only making the minimum monthly payments on a large balance, like a credit card debt. When you only pay the minimum amount due each month, it can cause your credit card balance to stretch out for years or even decades.

Example: A $1,000 balance on a credit card with an 18% annual percentage rate (APR) will cost about $684 in interest charges and take eight years to repay if you only make minimum payments of 3% of the balance.

“Compound interest is great when you are on the receiving end, but not when you are trying to pay down debt,” Hendrix says. “When interest is added to debt, you could end up paying interest on increasingly larger amounts.”

Five tips to maximize compound interest

1: Save early

Compound interest is not retroactive. In other words, you cannot earn compound interest on money that was not previously saved. The best time to become a first-time saver is when you receive your first paycheck. The second best time is today.

A useful tool to encourage saving is the 30-Day $100 Savings Challenge. After you save your first $100, “rinse and repeat” each month to grow the principal on which you receive interest payments.

2: Save as much as you can

Give compound interest as much “juice” as possible by powering up your savings deposits.

Increased savings may require earning a higher income via a new job, promotion, and/or side hustle. You can also find money to save by trimming expenses or earmarking windfall income sources such as tax refunds.

3: Save consistently

Keep adding money to your principal over a long period of time.

A great way to save consistently is automation. Here are two examples:

- Have your employer deduct savings deposits from your paycheck and direct them into a savings account.

- Transfer money from a checking account to a savings account using an app.

4: Save tax-deferred

Compound interest works best in tax-deferred retirement savings accounts such as an individual retirement account (IRA) or 401(k) or 403(b) plan. Earnings are not taxed until withdrawal, typically at retirement.

The longer savings grow free of taxes, the more time compound interest has to work its magic.

5: Pay off debt quickly

“Compound interest is bad when it comes to your debt, because it causes your debt to rise faster,” Bender says.

The secret to paying off debt quickly is to pay more than the minimum monthly payment. This will also save you money on the amount of interest you may owe and, therefore, the potential overall cost of the debt. For example, the $1,000 credit card balance noted above can be repaid in 4 years for $285 in interest by doubling payments to 6% of the outstanding balance. This is a savings of $399 over making minimum payments.

Of course, the best-case scenario, if you can afford it, is to pay credit card bills in full each month to avoid accumulated interest.

The bottom line

Many people don’t realize the awesome power of compound interest and their ability to build wealth without winning a lottery or receiving some type of windfall.

As the old saying goes, “Time is money.” Compound interest can be your friend or foe. The choice is yours.

Please note the below article contains links to external sites outside of OppU and Opportunity Financial, LLC. These sources, while vetted, are not affiliated with OppU. If you click on any of the links you will be sent to an external site with different terms and conditions that may differ from OppU’s policies. We recommend you do your own research before engaging in any products or services listed below. OppU is not a subject matter expert, nor does it assume responsibility if you decide to engage with any of these products or services.